စိတ်ကူးချိုချိုစာပေ

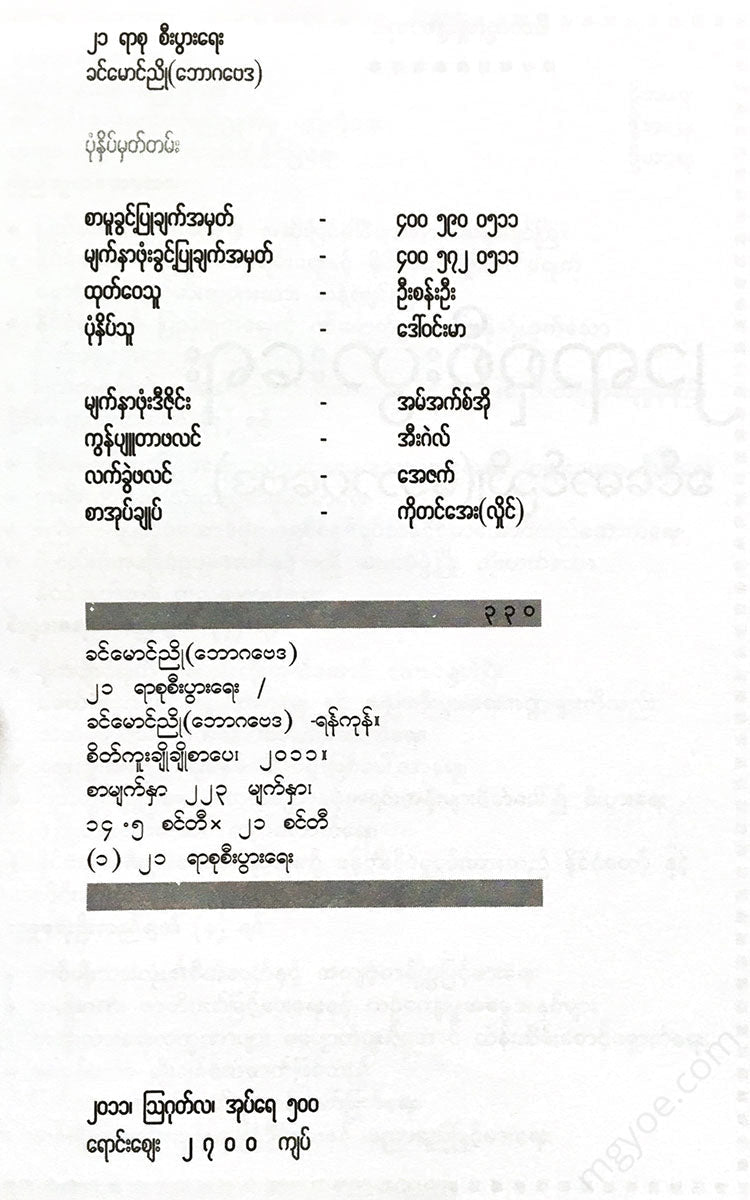

၂၁ ရာစု စီးပွားရေး

၂၁ ရာစု စီးပွားရေး

Couldn't load pickup availability

စာအုပ်အချက်အလက်များ

| စာရေးဆရာ | Khin Maung Nyo (Economics) |

|---|---|

| အမည် | ၂၁ ရာစု စီးပွားရေး |

| စာမြည်း | စာမြည်းဖတ်ရန်လင့် |

| စာအုပ်အမျိုးအစား | ပုံနှိပ်စာအုပ် — စီမံခန့်ခွဲ ၊ ခေါင်းဆောင်မှု |

| စာမျက်နှာ | ၂၂၃ |

| အရွယ်အစား | ၁၄.၅ စင်တီ ၊ ၂၁ စင်တီ |

| အလေးချိန် | ၂၄၀ ဂရမ် |

What is the fusion economy ?

The increasingly integrated global economy has created a completely new paradigm in the 21st century. Global warming, credit crunch, currency devaluation, food shortages, and trade wars are just a few examples of how economic factors, including the global economy, are changing our daily lives. Just as hydrogen molecules combine in a nuclear explosion and release a huge amount of energy, the increasingly integrated global economy is also releasing a lot of new energy, and we need to learn how to use that energy.

This new economic structure brings together forces and reactions that are impossible to understand using ordinary methods of analysis. In the past, economic conclusions were drawn based on simple logic. If a product is better or a company is more efficient, productivity increases. This means that everyone has a higher standard of living. Now it is not so easy to say. If the growth of China and India makes the world more polluted and food scarce, it is not good. If mortgages are accessible to everyone, and people borrow money to buy houses without being able to repay them, then it is good.

Billions of dollars in mortgage-backed securities are traded each year, and at one point the subprime debt market was even larger than the U.S. Treasury bond market, the largest market in the world. When banks and mortgage companies realized that they could transfer the risk of the mortgages they sold, they focused more on selling more, not caring about whether borrowers would be able to repay them. This loosened the rules for getting a loan, making it easier for poor and low-income borrowers to buy homes, and mortgages drove up housing prices. Many borrowers also bought homes they couldn't afford when prices rose, thinking they would be able to repay their loans.

When the housing market slowed, low-quality borrowers could no longer afford to pay their loans, let alone the interest on their original loans. As defaults on mortgages increased, the value of the bonds issued and sold based on subprime mortgages fell. As many subprime lenders went bankrupt, the price of subprime mortgages also fell.

Eventually, banks and investment firms that had bought the mortgage-backed securities were forced to repay, sometimes as much as 80% of the original value of the debt. This caused a global credit crunch, with other banks refusing to lend the money that companies and financial institutions needed to keep operating. Banks around the world were bailed out by cash-strapped governments. In the United States, the largest investment bank, Lehman Brothers, went bankrupt and was sold at a huge discount to its original value with the help of other investment banks, such as Bear Sterns, which were sold off by the Federal Reserve. The largest insurance company in the world, AIG, was also bailed out by the Federal Reserve. When the financial system began to collapse, there was no stopping it.

Subprime mortgages are :

At the beginning of the 21st century, when housing prices were high, banks and mortgage companies in the United States began to make loans to homebuyers who would not normally be able to get a loan. These “subprime” borrowers were able to borrow at a slightly higher interest rate than normal. Interest rates fluctuated depending on market conditions. These subprime loans were repackaged, resold as bonds, and then sold to investors around the world, including banks and financial institutions in Frankfurt, Germany, Tokyo, Japan, and Zurich. Many of the bonds were rated AAA, meaning they had the lowest risk of default. Unfortunately, many of these bonds were worthless, causing the collapse of banks, investment firms, and insurance companies around the world.

Collateral-backed security agreements are

The buyer of a home usually guarantees how much he owes the seller (I OWEYOU). Mortgage-backed securities are a type of mortgage-backed securities, or bonds, that are backed by assets such as mortgages or other collateral. In the early 21st century, subprime mortgages were repackaged and sold to investors as bonds. The sale was done with the understanding that the loans would eventually cover the value of the bonds. When housing prices fell more than expected, the mortgage-backed securities market collapsed, causing financial markets around the world to collapse. Banks and financial authorities around the world were forced to take on a variety of “toxic” mortgage-backed securities that could not be repaid.

In addition to the financial crisis, hurricanes and global warming are also influenced by the expanding economic structure of the 21st century. They bring together forces that are difficult to predict in the future. For example, the destruction of the Amazon rainforest for economic purposes is increasing the emission of carbon dioxide and methane into the atmosphere. In addition, the pollution produced by factories in the United States, Europe and China is rapidly melting the ice caps in the Arctic, warming the planet even more. This greenhouse effect is causing temperatures to rise in some parts of the world. No one knows when or where these events will end.

Efforts to reduce global warming by producing biofuels have also led to a number of unintended and unintended consequences. The production of sugar and corn-based biofuels uses a lot of water and reduces the amount of land available for human consumption, leading to shortages of rice, corn, and wheat on the world market, leading to riots in some countries and protectionism in others.

The converging global economy has also shaken up traditional patterns of trade and investment. For example, before the 21st century, most people bought and invested in local stocks and bonds. They waited patiently for their investments to appreciate in value. Today, pension funds, governments, and banks are buying and selling their money in a variety of complex insurance policies and investment vehicles.